Magazines urged to be more proactive and innovative in developing retail sales

Press sales, both magazines and newspapers, are coming under increasing pressure around the globe writes Jim Bilton, managing director of Wessenden Marketing, the marketing consultancy behind the new Distripress Circulation Monitor. Yet behind that stark – and obvious – headline, there lies a complex world. On one hand, the sales of print products are varying more and more widely from country to country and from sector to sector. On the other hand, the issues and business dynamics of press distribution are becoming increasingly similar: there are common problems (and common solutions) where different countries can learn from each other. It is these kinds of issues which the Distripress Circulation Monitor was set up to identify and tackle.

The key messages

The decline of print copy retail sales is accelerating in the face of massive digital disruption and of a slow, but clear shift from the retail channel into subscriptions. Yet the physical distribution of the international press remains a significant niche in global publishing with a 6% share of total press sales.

The key players in the supply chain have to be much more proactive at the front-end, particularly in protecting and developing retail display space rather than focusing purely on back-end processes or passively managing declining retail universes. Maintaining viable supply chains around the world is essential, but this needs to be done at the same time as stimulating the front-end consumer contact points.

Yet despite all the challenges, there are some growth markets. In addition, in the face of these pressures, the mood of the industry is actually relatively positive: one of steely realism rather than panic, with 39% of Distripress members seeing growth or stability in their businesses rather than decline.

The conclusion of the report is that it is time for the industry to manage the undoubted turbulence in the market more creatively rather than to be resigned to terminal decline.

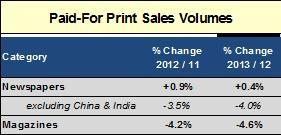

Topline volume trends

For newspapers, China and India are two massively important engine-rooms of growth, accounting for almost 50% of total global newspaper sales volumes between them. Strip these two influential markets out of the figures and the global newspaper business is in decline, accelerating in 2013 to -4.0% year-on-year.

Magazines have a completely different centre of gravity, with the largest market being the mature and declining Western Europe, which still accounts for over 40% of global sales volumes, but which dropped by 8.9% in 2013. The topline global picture for magazines shows the decline in 2013 accelerating to 4.6%, as fundamental structural change is really hitting the magazine business, some years after it started to impact on newspapers.

Magazine performance is also seeing much more variance than newspapers from sector to sector and from country to country. In addition, the magazine business model is very varied around the world in terms of such issues as the balance between advertising and circulation revenues and the impact of digital on print products.

The business of cross-border distribution

Looking behind the topline volume trends, the DCM assesses a range of the business issues. These include…

•The scale of the business. International, cross-border sales account for around 6% of the total sales of the 47 countries reviewed in the project – a significant niche in the modern press scene.

•General business performance. A steely realism informs the responses of the international operators involved in the Distripress member survey rather than panic. While the outlook is undeniably tough, with 61% of companies seeing their businesses declining currently, a significant 20% are experiencing growth in their business, with another 19% reporting that they are holding steady.

Opportunities and barriers to cross-border sales

Respondents gave their views as to what is driving and holding back subscriptions and digital sales, but for retail the key opportunities are seen to be…offering a wider range of titles to meet consumer needs…and having more retailers and more space within those retailers, with travel points, non-traditional outlets and independents highlighted for more focus for international products. The key barriers are felt to be…the growth of digital…and the reduction in retail numbers and retail shelfspace for press products.

As one Distripress member put it: “Our industry is not very innovative or proactive. Change usually only happens due to retailer pressure rather than our initiative. We have to change that mentality to survive. We have to take control of our own destiny. Yet we can’t do that on our own.”