M&A market finishes strong in 2015, outpacing 2014 deal volume and value

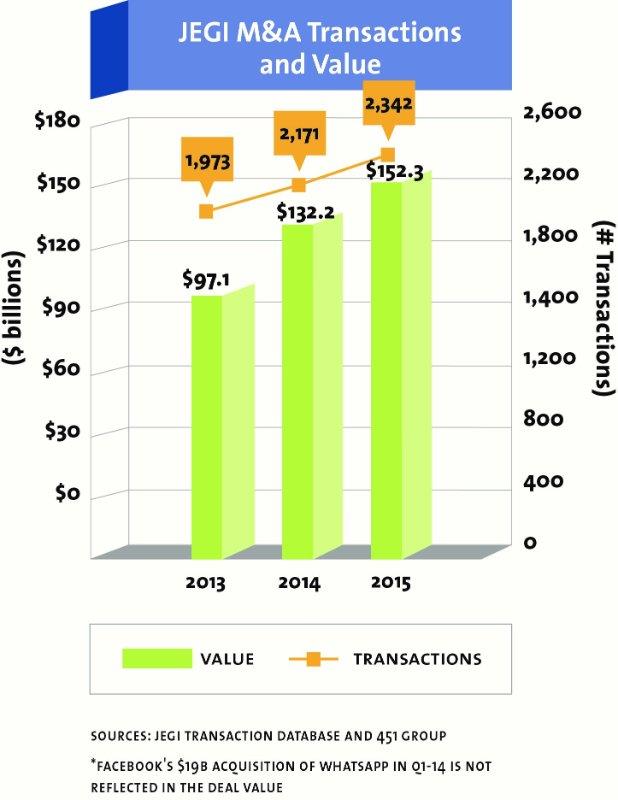

Both deal volume and value showed solid gains over 2014 results, increasing 8 per cent in number of deals and 15 per cent in value year-over-year. With the surge in M&A continuing, deal activity approached levels not seen since the pre-recession period in 2007, according to JEGI, the leading independent investment bank serving these core markets.

Software & Tech-Enabled Services

The most active sector for M&A was Software & Tech-Enabled Services, which accounted for more than half the deal volume and value, with 1,441 transactions totalling $76.3 billion.

Corporations are investing heavily to grow their software and technology capabilities through M&A, given the fast-paced evolution in cloud-based technologies and the increasing convergence across media, marketing, data and technology. In addition, private equity investment continues to expand in software and technology, in line with PE firms’ healthy appetite for businesses with recurring revenue models.

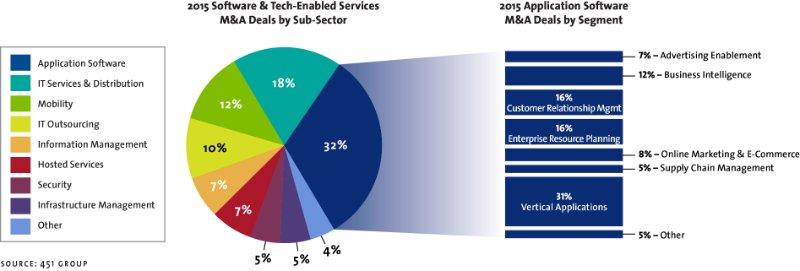

The chart on the left in the attached PDF shows a breakdown of deal volume by sub-sector within this red-hot sector. Application software was the most active sub-sector, accounting for nearly one-third of the Software & Tech-Enabled Services sector deals. Other active sub-sectors were IT services & distribution (18 per cent of the deals), mobility (12 per cent), IT outsourcing (10 per cent), hosted services (7 per cent), and information management (7 per cent).

The chart on the right in the attached PDF shows a further breakdown of the segments within the application software sub-sector. Vertical applications accounted for the highest deal volume (31 per cent), followed by customer relationship management (16 per cent), enterprise resource planning (16 per cent), and business intelligence (12 per cent).

Mega Deals in 2015

Twenty-nine M&A transactions across the media, information, marketing, software and tech-enabled services sectors surpassed $1 billion valuations in 2015. The Software & Tech-Enabled Services and Consumer Media & Technology sectors accounted for 18 of the 30 largest transactions.

JEGI Closings in Q4 2015

JEGI was very active in 2015, with 20 announced deal closings, as well as a number of pending transactions. In the fourth quarter of 2015, JEGI announced five deal closings:

- The sale of Imago Techmedia, a leading enterprise technology tradeshow organiser, to Clarion Events, a portfolio company of Providence Equity Partners (JEGI and its UK investment banking partner, Clarity, advised Imago);

- The sale of Opus Agency, a global corporate events and experiential marketing agency, to Fan Creek Capital;

- The sale of The Nielsen Company’s National Research Group (NRG), a provider of research and analytics to the entertainment industry, to The Stagwell Group via its fund Stagwell Media LLC;

- The sale of World 50, an exclusive, invite-only peer-to-peer network and knowledge exchange platform serving senior executives at leading corporations, and a portfolio company of Chicago Growth Partners, to Pamlico Capital; and

- The sale of FC Business Intelligence’s TU Automotive, the global leader in the B2B automotive technology events and information sector, to Penton Media, a portfolio company of MidOcean Partners and Wasserstein & Co. (JEGI advised FCBI with Clarity, highlighting the fourth joint deal closing for the partnership in 2015).

Looking Ahead to 2016

As we look to the year ahead, we are facing global uncertainty, with volatility in stock markets worldwide, due to interest rate increases, the economic state of China, and an upcoming US presidential election, as well as lingering fear following terrorist attacks in Paris and San Bernardino, California and insecurity throughout Europe from the ongoing refugee crisis.

However, the US M&A market has continued to flourish, proving to be an economic bright spot in an uncertain global economy. Despite the widespread uncertainty, the US continues to see a stable domestic economy, driven by low unemployment, robust debt markets, and strong corporate investment. Global corporations and private equity firms are continuing to invest in M&A, given unprecedented capital reserves and the need for growth. While we are still wary of the global economy’s potential impact on deal-making, we expect M&A to remain very active through 2016.

M&A Highlights in 2015

The b2b media and technology sector deal volume was down from 103 transactions in 2014 to 93. Deal value, however, rose slightly to $6.2 billion, up from 2014’s $6.1 billion. Notable Q4 2015 transactions included the: SFW Capital Partners $212 million growth investment in Gerson Lehrman Group, an online platform for professional learning and expertise; All Web Leads acquisition of Insurancequotes.com and NetQuote from Bankrate, online marketplaces for purchasing insurance products and services, for $165 million; and GateHouse Media acquisition of Dolan Company’s Business Information Division, which publishes business and court journals, as well as commercial newspapers, for a reported $46.5 million.

The consumer media and technology sector’s deal volume dropped slightly to 201 transactions in 2015, down from 206 deals in 2014. Deal value rose substantially, however, up 60 per cent to $26.9 billion, due to several transactions crossing the $1 billion threshold in 2015, including Alibaba’s $4.4 billion acquisition of an 80 per cent stake in Youku Tudou, a Chinese Internet television company, and Expedia’s $4.3 billion acquisition of vacation rental property marketplace HomeAway, both in Q4. Other notable deals from the fourth quarter of this year were Pandora Media’s $480 million acquisition of Ticketfly, a cloud-based integrated social marketing and ticketing platform for events and venues, and Gannett’s acquisition of Journal Media Group, which operates as a media company with print and digital publishing activities, for approximately $300 million.

The database and information services sector announced 59 deals in 2015, down from 70 deals in 2014. Deal value, however, rose nearly threefold, to $19.4 billion, vs. 2014, due in large measure to Q4’s mega transactions: Intercontinental Exchange’s $7.8 billion acquisition of Interactive Data Holdings; IBM’s $2 billion acquisition of Weather Company’s Product and Technology Business; and Equifax’s $1.9 billion acquisition of Veda Group. Other notable deals in Q4 2015 included Bloomberg’s acquisition of Barclays’ Risk Analytics and Index Solutions business, which provides benchmark and strategy indices, portfolio analytics and risk models, for approximately $775 million, and IHS’s acquisition of CarProof, provider of used vehicle history reports, for $468 million.

The exhibitions and conferences sector saw a sharp increase in deal volume, with 86 transactions in 2015 vs. 53 in 2014. Deal value more than tripled to $3.7 billion in 2015, led by Q2’s $1.2 billion acquisition of Cirque du Soleil by a group of investors, and the Dalian Wanda Group acquisition of World Triathlon Corporation, owner and organiser of the Ironman triathlon events, from Providence Equity Partners for $650 million in Q3. Notable transactions for Q4 2015 included the: Pamlico Capital acquisition of World 50, an exclusive, invite-only peer-to-peer network and knowledge exchange platform serving senior executives at leading corporations (JEGI represented World 50); Fan Creek Capital acquisition of Opus Agency, a global corporate events and experiential marketing agency (JEGI represented Opus); and Penton Media acquisition of TU Automotive from FC Business Intelligence (JEGI represented FCBI).

The marketing services and technology sector continues to be very active, with deal volume increasing in 2015 to 631 deals vs. 2014’s 602 deals. Deal value, however, decreased to $26 billion, down from $39.7 billion in 2014, due to several mega deals in 2014 that were not matched in size in 2015. Notable transactions for the fourth quarter of 2015 included the:

- Endurance acquisition of Constant Contact, an all-in-one marketing platform for organisations to create email and online marketing campaigns, for $1.1 billion

- Cision/GTCR acquisition of PR Newswire, provider of news distribution, targeting, monitoring and marketing solutions for companies to connect and engage with target audiences, from UBM for $841 million

- NeuStar acquisition of MarketShare, provider of marketing analytics solutions for businesses, media companies, marketers and agencies, for $450 million

- STW Media Services acquisition of WPP’s Australia and New Zealand marketing and advertising services businesses for approximately $310 million

- DDB Worldwide (subsidiary of Omnicom Group) acquisition of Grupo ABC, a Brazilian agency providing advertising, specialised marketing, content and entertainment services, for $270 million

- IDI acquisition of Fluent, provider of integrated performance marketing solutions for the digital domain, for a reported $225 million

- Perion Network acquisition of Undertone Networks, provider of cross-screen digital advertising solutions, from JMI Equity for $180 million

- Tyco International acquisition of ShopperTrak RCT, provider of shopper insights and analytics solutions improving retail profitability and effectiveness, for $175 million

- Deluxe Corp acquisition of Datamyx, provider of risk-based data-driven marketing solutions, from Halyard Capital for $160 million

- Sabre Corporation acquisition of Trust Group of Companies, provider of marketing, distribution and training services for hotel groups, for $154 million

- Veeva Systems acquisition of Zinc Ahead Holdings, provider of marketing compliance solutions for the life sciences industry, from Accel-KKR for $127 million

- The Stagwell Group acquisition of National Research Group (NRG), a provider of research and analytics to the entertainment industry, from The Nielsen Company (a JEGI transaction)

M&A activity for the mobile media and technology sector rose in both number of deals announced and value in 2015, to 148 transactions and $6.5 billion vs. 2014’s 141 deals and $5 billion. The rise in deal value was mainly due to the Audi, BMW and Daimler acquisition of Nokia’s HERE for $3.1 billion in Q3. Notable Q4 2015 deals included: RNTS Media’s acquisition of Heyzap, provider of mobile advertising for app developers, for $45 million; LOV USA’s acquisition of Smooch Labs, creator of Jewish dating app JSwipe, for $17 million; and Microsoft’s acquisition of Mobile Data Labs, provider of mileage-tracking app MileIQ, for an undisclosed amount.

The software and tech-enabled services sector increased in both deal volume and value, with 1,441 transactions totalling $76.3 billion for 2015, compared to 2014’s 1,436 transactions at $73.8 billion. Notable transactions in the fourth quarter of 2015 included the: Global Payments acquisition of payments processing company Heartland Payment Systems for $3.8 billion; Roper Technologies acquisition of Aderant Holdings, provider of legal practice management software, from Madison Dearborn Partners for $675 million; Blucora acquisition of HD Vest, provider of financial BPO SaaS and services, from Parthenon Capital Partners for $580 million; and CoreLogic acquisition of FNC, provider of property appraisal management software, for $475 million.

More like this

Digital media mergers & acquisitions predicted to pick up in 2015

TU Media accelerates digital first transformation with acquisition

Meredith continues digital drive with acquisition of Grocery Server